If you’re a sole trader who uses a car or other motor vehicle as part of running your business, you should absolutely be claiming motor vehicle expenses. It’s a no brainer!

Motor vehicle expenses are the most common expense type raised through the Hnry app, and we love to see it – claiming everything you’re eligible for is a great way to get tax relief.

Let’s get started!

What motor vehicle expenses can you claim?

Great question!

The good news is that you can claim almost all expenses related to the business use of your vehicle (although it’s slightly different depending on your claiming method).

This includes things like:

- Petrol

- Maintenance costs

- Road user charges

- Parking and toll fees

- Insurance

- Registration inspection

- Depreciation

💡 You can’t claim any fines, parking tickets, or towing fees you incur, even if they’re earned while you’re on the job. Sorry!

It’s important to note that only the business usage of your vehicle is eligible for tax deductions. Personal trips, like a quick trip to the shops, or a weekend roadie with the boys, can’t be claimed.

So –

What exactly is “business use” for a sole trader?

If you’re using your vehicle in connection with your business activities, it might qualify as business use.

But there’s a catch: Trips between your home and your regular place of work are classed by the ATO as personal travel, ruling out any deductions – unless you have a home-based business and are travelling for work-related reasons.

“Business use”

You may be eligible to claim a tax deduction for travel expenses in your vehicle when you:

- Travel from your usual workspace to another work location (for instance, a client’s office) while working.

- Head from home to an irregular work spot to carry out tasks (this doesn’t count if the alternate spot becomes a regular workspace).

- Deliver goods or fetch materials

- Attend work-related conferences or gatherings outside your usual location

- Commute between distinct job locations, especially if you have multiple roles

“Business use” for home-based businesses

The ATO has strict requirements for classifying a business as “home-based”. For starters, you’ll need to have “an area of your home set aside as your ‘place of business’ that cannot readily be used for personal purposes”. A desk in a guestroom might not cut it!

You might qualify as having a home-based business if:

- It’s clearly identifiable as a place of business – eg. you have a business sign outside the front of your house

- The area you work from is not readily suitable or adaptable for private or domestic purposes

- It’s used exclusively or almost exclusively for carrying on your business

- It’s used regularly for visits from clients.

💡 For more information on home-based businesses, head over to the ATO website.

If, and only if, you qualify as a home-based business, then journeys between your home and other destinations are deductible if they’re work-related.

Here are some scenarios where travel costs might be claimable:

- Visits to a client’s location to perform work or drop off documents

- Store trips to buy equipment or inventory

- Going to the bank for business transactions

- Heading to the post office to send out invoices or check your PO Box

- In-office consultations with your business tax agent or BAS agent

But, if you’re taking a trip to the supermarket to pick up snacks and frozen pizza for your birthday party – no dice!

Which vehicles qualify for tax deductions?

The short answer: all of them!

But how you claim vehicle expenses will depend on what kind of vehicle you drive (we’ll cover this in just a sec).

The ATO categorises vehicles as either “cars” or “other vehicles”, and are surprisingly specific about what’s what.

Cars

For your vehicle to be considered a car for tax purposes, it can’t be able to transport more than 1 tonne, or more than 8 passengers excluding the driver.

Also, to state the obvious, motorcycles and their equivalents aren’t considered cars.

You’ll need to own or lease the car, to be eligible for a tax deduction. If you’re using a relative’s vehicle through a private arrangement, you can still claim running expenses as if the car belongs to you (using the actual costs method only though).

Other vehicles

The following vehicles don’t fall under the ‘car’ category:

- Motorcycles

- Scooters and similar vehicles

- Vehicles with a cargo capacity of more than 1 tonne (like large trucks and some utes)

- Vehicles made for 9 or more occupants, including the driver (like some vans and minibuses).

How to claim car and other vehicle expenses

As a sole trader you can choose from different methods to claim a tax deduction, depending on your vehicle type.

- For cars, you can opt for either the cents per kilometre method or the logbook method (more on that below).

- 💡 Note: If you’re going the cents-per-kilometre route, you can’t claim your car’s depreciation as it’s already included in this method!

- For vehicles that aren’t cars, you have to use the actual costs method.

Let’s take a deeper dive into each one:

Cents per km method (car only)

To use the cents per kilometre method, multiply your business-related kilometres covered by the rate per kilometre for that financial year, which is 88 cents for the 2024/25 and 2025/26 financial years. You can only claim up to 5,000 business-related kilometres ($4,400) for each car.

This method includes all car expenses, meaning you can’t claim any other additional vehicle expenses – including depreciation or fuel.

While receipts aren’t mandatory, you should have a way to validate your ownership of the vehicle and the business nature of trips – for example, keeping a record of these in a diary.

The cents per kilometer method doesn’t require you to keep a logbook to show exactly how many kilometres you travelled, however the ATO may ask you to show how you worked out your business kilometres – like those diary records.

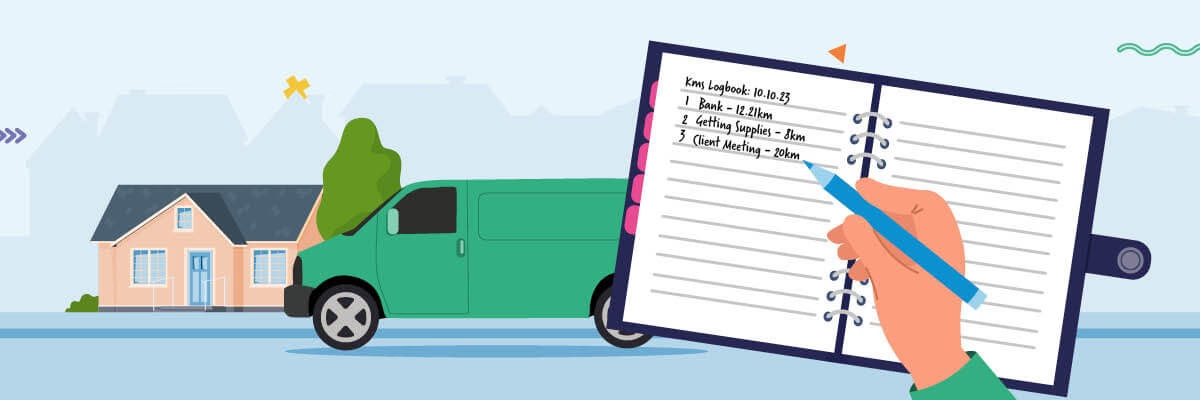

Logbook method (car only)

A logbook is simply a document that ‘logs’ relevant data regarding your business-related trips. It needs to cover a minimum of 12 consecutive weeks and represent your typical usage for the financial year.

Make sure you record:

- Where you’re going and why for each trip

- Odometer readings at the beginning and end of every journey

- Total distance in kilometres you’ve travelled in that period

- Odometer readings for the beginning and end of the logbook period.

After you’ve completed your logbook, you need to work out how much you used your vehicle for business, based on the information you collected:

- Determine the total distance in kilometres you travelled during the logbook duration.

- Identify the business-related kilometres within that timeframe.

- To find the business usage percentage, divide the business-related kilometres by the total distance and multiply by 100.

- Total up all allowable motor vehicle expenses for the claim duration.

- Your claimable amount is the business usage percentage of your total expenses.

💡Note: Even if you use your vehicle for work 100% of the time, you need to prove this to the ATO, which is why you still need to keep a logbook.

In addition to business-related journey details, you also need to keep:

- Receipts for fuel and oil (or an estimate of these based on your odometer readings)

- Receipts for other car-related costs such as registration,

- insurance,

- lease payments,

- services,

- tyres,

- repairs, and

- interest charges (phew!).

- Details about the car’s purchase price and how its depreciation was calculated (we’ll get to this bit in a moment).

Actual costs method (all other vehicles)

For vehicles that aren’t classified as cars, or aren’t owned by you, you need to use the actual costs method.

You’ll need to:

- Calculate your actual expenses for work-related trips

- Claim the deduction in your tax return as a work-related travel expense (not as a work-related car expense).

Although the cents per kilometre and logbook methods aren’t applicable here, keeping a logbook-type record helps in establishing your business usage percentage.

It’s not required, but it is a good way to show how you calculate your work-related trips.

How to claim your vehicle purchase

💡 Note: If you’re using the cents per kilometre method to claim vehicle expenses, you can’t double-dip by also claiming the vehicle’s purchase. It’s already baked into that deduction!

You can claim the cost of your vehicle in two ways:

- Instant asset write-off

- Depreciation

💡Remember: You’ll need a logbook tracking at least 12 weeks worth of trips in order to calculate your business use percentage of your vehicle. Like with all other vehicle costs, you can only claim the business usage of your vehicle purchase.

Instant asset write-off

If you bought your vehicle between 1 July 2024 and 30 June 2025, and its cost doesn’t exceed $20,000 (the current instant asset write-off threshold for the 2025/26 financial year), you can claim the business use percentage of its cost immediately as a deduction.

Depreciation

Assets like vehicles decrease in value over time. This reduction is called depreciation. If your vehicle costs more than $20,000 and is purchased (and available to use) before 30 June 2026, you may want to claim depreciation on the purchase.

💡Note: You can still only depreciate your business-use percentage of the purchase of your vehicle. For instance, if your business use of a $60,000 car is 80%, you can claim depreciation on $48,000 (80% of $60,000). If you bought the vehicle before 1 July 2023, different regulations might apply.

📖 For details on how to depreciate assets, take a look at our sole trader guide to depreciation.

What’s the cap on car-related depreciation?

For the financial year 2025/26, if the vehicle is a car, the maximum deductible amount based on its price is $69,674.

Tricky stuff, right? It’s best to consult professionals on this. Like Hnry - it’s exactly what we’re here for, to make those depreciation calculations for you.

Let Hnry take the driver’s seat (for your deductions)

Trying to get your head around tax deductions is like navigating through a maze without a map.

Why get stuck with numbers when Hnry can cruise through them effortlessly?

We’re an award-winning app specifically for sole traders, so we get you. With Hnry at the wheel, you can relax, knowing we’ll take care of all the complicated calculations and ensure you get back every dollar that you’re entitled to.

For just 1% + GST of your self-employed income, capped at $1,500 a year, Hnry will calculate and pay all your taxes, levies and whatnot for you, including:

Let Hnry take the driver’s seat on your tax admin, so you can focus on what you do best – the actual work.