In a perfect world, claiming tax deductions would be simple.

But, we live in the real world, where the tax rules are (necessarily) complex. Not every purchase you make on behalf of your business is tax deductible, unfortunately. The good news is that you’re probably not claiming everything you can claim!

Research shows that a whopping 36% of sole traders with business expenses don’t claim all the tax deductions they’re entitled to. That’s an average of $5,611 in unclaimed deductions per sole trader, per financial year – which is straight-up mind-blowing.

To help sole traders navigate the metaphorical wild west of tax deductions, the ATO have come up with three golden rules for making claims. If your expense meets these three requirements, it’s *possibly* tax deductible:

- The expense must have been for your business, not for personal use.

- If the expense is for a mix of business and personal use, you can only claim the portion that is used for your business.

- You must have records to prove it.

On top of these three rules, there are a few other guidelines to bear in mind as an NDIS support worker:

- You can only claim what you’ve paid for out of pocket. If your client/employer reimburses you for an expense, it’s no longer claimable.

- The exception is allowances. If you receive an allowance for an expense (eg. travel), and you spend it on that expense (e.g. travel), you can claim it as an expense.

To help you make heads AND tails of it all, we’ve put together a quick cheat sheet for 15 NDIS-worker expenses that you can claim, might be able to claim, and can’t claim.

We’ve also included a few guidelines explaining why an expense will/may/won’t be accepted by the ATO.

Let’s get claiming!

Key:

- ✅ - straightforward and claimable

- ⚠️ - claimable if certain conditions are met

- ❌ - not claimable at all. Sorry folks.

Can claim:

1. Fees and insurance 2. Protective items 3. Seminars, conferences, and training courses 4. Tools and equipment 5. Travel expenses 6. Working from home expenses

Might be able to claim:

7. Car expenses 8. Clothing and laundry 9. Driver’s license 10. Meals 11. Self-education and study

Can’t claim:

12. Child care 13. Entertainment and social functions 14. Glasses 15. Grooming costs

Expenses NDIS Workers can claim

1. Fees and insurance ✅

All professional fees and insurance payments are claimable including union fees, professional association fees, and the cost of getting your blue card. Make sure you claim them all!

2. Protective items ✅

Protective items (gloves, hand sanitiser, PPE, non-slip shoes, sunscreen if working outside) are all claimable, but only if your employer doesn’t reimburse you.

3. Seminars, conferences, and training courses ✅

Like with education, costs for seminars, conferences, and training courses that will help you get ahead in your current role are tax deductible.

Better yet, travel expenses, accommodation, and meals are all also tax deductible if you’re required to stay away from home for more than a day. Whoohoo!

You just need to make sure that the whole trip is 100% work related. You can’t fly to Bora Bora for a holiday, attend a seminar on aged care, and then expense the entire trip (unfortunately). In this case, only direct costs like the seminar registration fees will be tax deductible.

Zafeer is a disability support worker from Melbourne who struggles to keep on top of his finances. After miscalculating his taxes and incurring a hefty fine from the ATO, his agency recommends he attend a free basic bookkeeping seminar for NDIS workers. Zafeer decides to go, driving three hours to the seminar’s location, and staying in a motel overnight. Unfortunately, he is unable to claim any costs for the trip because the seminar didn’t directly relate to his ability to do his job. He did, however, sign up for Hnry, and never missed another tax payment again 😉.

4. Tools and equipment ✅

Any equipment you need in order to do your job (mobile phone, disability ramp, stethoscope) is tax deductible. Remember though: If the equipment is for both business and personal use, you can only claim the business portion of the cost.

5. Travel expenses ✅

Like with seminars, conferences, and training courses, you can claim any costs associated with an overnight trip for work. The exception is if you’re staying overnight at a client’s house; the ATO doesn’t consider this a travel expense.

If you receive an allowance for overnight costs, and this allowance is part of your assessable income, you can still claim these expenses if you can show:

- You were away overnight

- You spent money while away

- The trip directly relates to earning income

- How you worked out your claim

Got all that? You’re golden☀

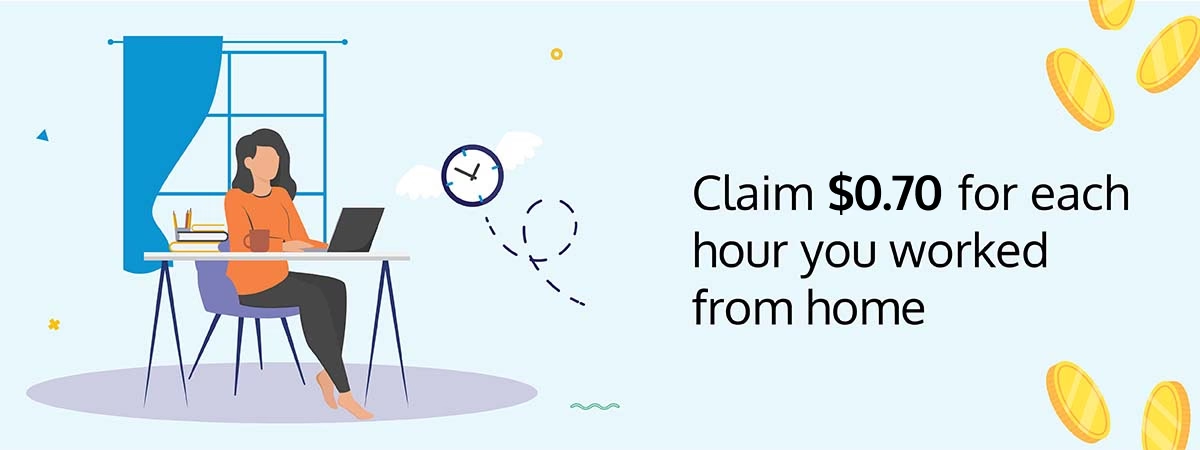

6. Working from home expenses ✅

There are two ways to calculate your WFH expenses. Each has its own pros and cons, and the one that’s best for you will depend on your situation.

- Fixed rate method - for those who are short on time

- Actual cost method - for those who have a big, dedicated space for working from home

Fixed rate method

To use the fixed rate method, you need to have:

- A dedicated, separate space for working from home

- A log/timesheet of the number of hours you spend working from home across the financial year

From there, you can claim the fixed rate of $0.70 (from 1 July 2024) for each hour you worked from home. This covers:

- The decline in value of home-office furniture, like a desk

- Electricity and gas for heating, cooling, and lighting

- Cleaning costs

Using the fixed rate method means that you can’t claim any of these costs separately. You can however claim the work-related percentage of other expenses that aren’t covered by the $0.70 rate (from 1 July 2024), like:

- Phone, data, and internet expenses (including the decline in value of your mobile phone!)

- Computer accessories and stationery

- The decline in value of other office assets

💡 For more information about claiming the decline in value of your assets (including what an asset actually is), check out our monster article on expenses.

Actual costs method

With the actual costs method, you work out your expenses by multiplying relevant costs (all costs mentioned in the “fixed rate method” section) by the percentage of your home that forms your home office.

To use this method, you’ll need:

- a record of the number of hours you work from home in an income year OR a 4-week diary recording your usual work-from-home pattern.

- receipts, bills, or other documents recording the running expenses you include in your expense claim.

Expenses you may be able to claim

7. Car expenses ⚠️

Car or motor vehicle expenses are tax deductible, but only in specific circumstances:

- ❌ You CAN’T claim the cost of normal trips between home and work, even if you work outside of usual business hours. This includes any taxi or public transport fares; the ATO considers your regular commute a private expense.

- There are limited exceptions to this rule. For example, if you have no fixed place of employment and you continually travel from one work site to another.

- ❌ You CAN’T claim any tolls you pay driving between home and your regular place of work.

- ❌ You CAN’T claim parking costs for parking at or near your regular place of work.

- ✅ You CAN claim the cost of driving from one job to another during the working day.

- ✅ You CAN claim the cost of driving between alternate work locations for the same employer eg. if you take a client to an appointment.

- ✅ You CAN claim the cost of tolls and parking on work related trips.

Sunny is an aged care worker. She drives from her house to her first client Joy’s house, and they have breakfast together. She then takes Joy to a physio appointment, where she pays $3.00 to park her car. After dropping Joy home, Sunny then heads to her second client Sarah’s house, incurring a $2.00 toll on the drive over. Sarah and Sunny have some afternoon tea, go for a walk, and play a quick round of Just Dance on Sarah’s Nintendo Switch (a recent gift from her grandchildren). As the sun sets, Sunny says goodbye and drives home. Aside from the drive to work (from home to her first client Joy’s house), and the drive home again (from second client Sarah’s house), Sunny can claim all trips, parking fees, and tolls as business expenses.

Claiming car expenses

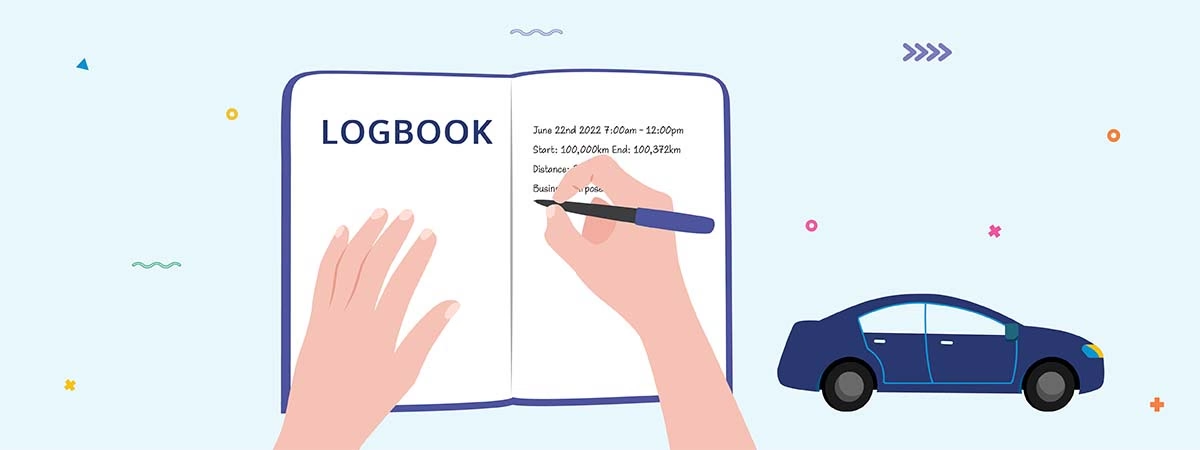

To claim the cost of car expenses, you can use either the logbook method or the cents per kilometre method.

Logbook method

The logbook method is used to calculate the business-use percentage of the expenses for the vehicle. Expenses include fuel, maintenance, and registrations.

To work out your business-use percentage, you’ll need to keep a logbook (obviously) for a minimum of 12 continuous weeks. Note the income year you create the logbook, and then for each trip you take, record:

- the date the journey began, and the date it ended

- the car’s odometer reading at the start and end of the journey

- how many kilometres the car travelled on the journey

- why the journey was made (eg. for business or personal reasons)

Once your logbook is complete, you can work out the percentage you use your car for work, and claim that percentage of all running expenses. Unless your circumstances change significantly (eg. you change jobs), your logbook will be valid for five years.

You can claim fuel and oil costs based on your actual receipts, or you can estimate costs based on your odometer readings. For all other expenses, you’ll need written proof (eg. WoF, maintenance etc).

💡 If the cost of fuel skyrockets unexpectedly, using the logbook method means your fuel claims will keep pace with the pump price. It might be worth the admin if you use a lot of petrol for work.

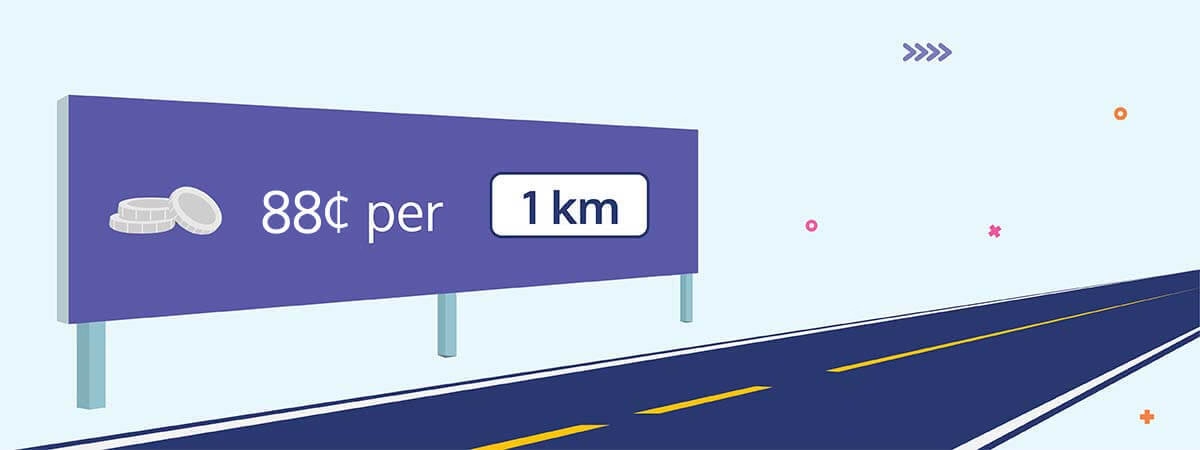

Cents per kilometre method

For the 2024/25 and 2025/26 financial years, you can claim $0.88 per kilometre for every tax-deductible trip you take, up to a maximum of 5,000km (or $4,250).

For the 2024/25 and 2025/26 financial years, this rate goes up to $0.88 per kilometre, up to 5,000kms (or $4,400).

You won’t need to keep a logbook, but the ATO might ask you to show them how you calculated your business kilometres. It’s far easier, but less accurate than using a logbook.

| Logbook method | Cents per kilometre method |

|---|---|

| Pros: • Potentially a bigger deduction, if your vehicle expenses are high. | Pros: • Low admin |

| Cons: • More admin | Cons: • Potentially a lower deduction, if your vehicle expenses are high |

📖 For more on claiming vehicle expenses, check out our guide for sole traders.

8. Clothing and laundry ⚠️

This one’s a bit tricky. The ATO only allows deductions for:

- uniforms with logos,

- occupation-specific clothing (eg. nurse scrubs),

- and unconventional costumes (eg. a clown suit if you work as a clown).

Even if you only use certain clothes for work, if they could feasibly be worn outside of work, you’re out of luck.

If your work clothes ARE tax deductible however, you can also claim the related laundry expenses. This includes:

- Dry cleaning and repairs.

- $1 for every load containing just your work clothes.

- $0.50 for every load containing a mix of work and personal garments.

If your laundry expenses (minus dry cleaning) are less than $150, you don’t need to keep records to prove your costs, but you will need to be able to show how you calculated and worked out your claim.

9. Driver’s licence ⚠️

While you can’t claim the cost of getting or renewing your regular driver’s licence, you can claim the costs for any additional special licences or conditions you need for work.

For example, a heavy vehicle permit needed to drive a retirement-home bus is a claimable work expense.

10. Meals ⚠️

- ❌ You CAN’T claim the cost of food, drinks, and snacks consumed during normal work hours, even if you receive an allowance. These are considered private expenses.

- ✅ You CAN claim meals bought when working overtime IF you receive an overtime meal allowance, and this allowance is included in your assessable income.

- 📖 Your assessable income is the income you pay taxes on. For more information, read our article on how taxes work.

- ✅ Similarly, you CAN also claim meals you buy when travelling overnight on a work trip (memo to self: remember this burger next time you’re in Perth for work).

11. Self-education and study ⚠️

You can claim all self-education and study expenses IF your course relates directly to your current role. In order these expenses to be eligible, your education needs to:

- Maintain or improve the specific skills and knowledge you need for your current duties

- Be likely to result in an increase in income from your current employment.

You can’t claim a deduction for a course that will help you get a new job, or if it’s only tangentially related to your line of work. Personal development courses unfortunately don’t cut the mustard with the ATO.

Expenses you can’t claim

12. Child care ❌

Even if you aren’t able to work without paying for childcare, childcare is considered a personal expense. It’s never claimable (sorry).

13. Entertainment and social functions ❌

This one’s a bit of a hard pill to swallow, we won’t lie. Entertainment and social event costs are considered personal expenses, even if they’re related to work. Even if they’re required for work. It’s not tax deductible to:

- Take your client to a movie.

- Take your client out for a coffee.

- Attend a networking event (even if your recruitment company says it’s compulsory for you to be there - ouch!).

14. Glasses ❌

The ATO doesn’t care if you’re as blind as a bat without them; glasses are a personal expense.

15. Grooming costs ❌

Your recruitment company might need you to be well turned out 24/7, but the ATO likes you just the way you are. Grooming costs are considered personal expenses.

Claim tax deductions with Hnry

Research shows that NDIS workers spend an average of 9 hours a week and $391 a month on tax and financial admin. That’s way too much! In contrast, Hnry users spend an average of 2 hours a week, and our fee is 1%+GST of your self-employed pay, capped at $1,500+GST annually.

In short: we may be biased, but we reckon the best way for NDIS workers to maximise tax deductions (cost-effectively and legally!) is to use Hnry.

Hnry is an award-winning app that’s helping NDIS workers spend less time on financial admin, and more time doing what they love (unless what they love is financial admin). Once you’re up and running with Hnry, we’ll automatically deduct all relevant tax payments and levies every time you’re paid, so you won’t accidentally end up with a massive tax bill at the end of the financial year. We’ll even lodge your annual tax return for you, at no additional cost.

Raising expenses through our app is as simple as taking a photo of your receipt and inputting a few extra details. From there, our accountants will manage all your tax deductions, so you get the right tax relief back in real time (rather than having to wait until the end of the financial year). Easy as!

Get your tax ducks (and deductions) in a row by joining Hnry today!